For the blockchain market, comparisons to the Internet abound, especially on whether the dot Com crash of 2000 will bear similarities to its blockchain cousin. A simple analogy would lead you to believe that since we are probably around the 1997-1998 time-frame in relation to Web chronology, when we cross into 2000, a similar crash might happen. For that class of believers, they would have you sit out the current blockchain activity, wait for an imminent blockchain crash, and then pick up its pieces, just as you might have done with the Internet, post 2002 when the post dot-com bear market ended. But that argument doesn't necessarily hold a lot of water in the blockchain space because of the thesis of this post:

Rather than one big crash that resets the entire field, there will likely be a succession of mini crashes, one following the other. Each one of these mini crashes will flush some bad coins, while simultaneously bringing new ones, and giving birth to new projects of increasingly higher quality.

So, if you are waiting for a big blockchain crash, it may never happen as such, because it is already happening in smaller (yet significant), successive doses. It’s like death by a thousand cuts. More importantly, if you are a venture investor, skipping this period would have you miss the opportunities that continue to emerge, as well as miss the learning experiences which only come from being directly involved in something. Furthermore, while the Internet crash of 2000 put a temporary chill on the funding of new tech companies, the blockchain’s market cap volatility is barely affecting the pace of startup innovation and open sourced decentralization projects that are getting funded.

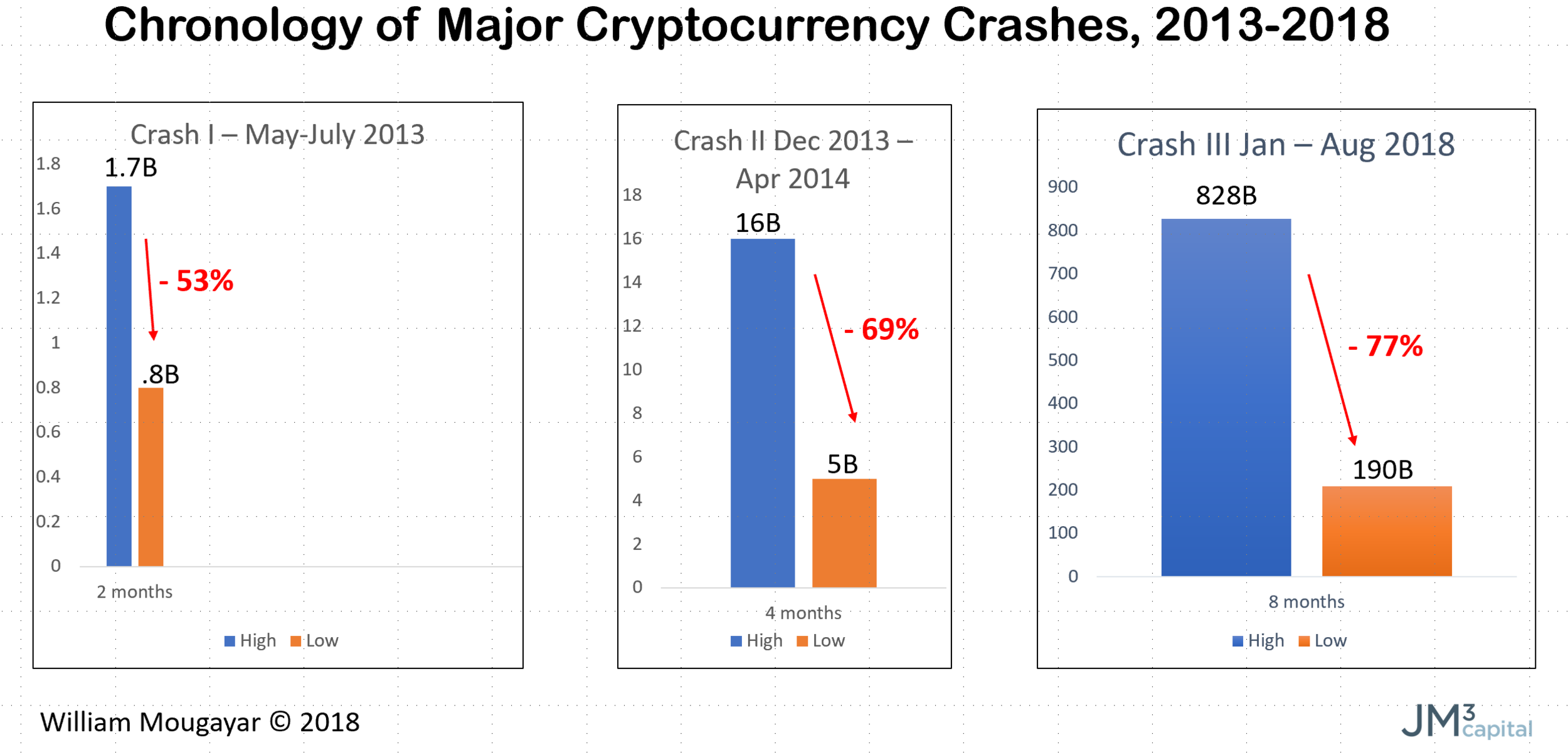

If you look at the recent market highs of January 2018 (and December for Bitcoin specifically), and compare to where we are today, you will see that we already have seen the equivalent of a crash in terms of market capitalization losses, across the board. The low of $190B on Aug 14th 2018 is about one quarter of the market value high of $828B that was attained in January. Many coins are currently trading at 10-20% of their highest value. And there were other crashes prior, when market caps lost billions again. Here's a chronology:

It is interesting to note that while the first crash took place over a 2-month period, the second one took 4 months to materialize, and the current one has been 8 months in the making. Maybe there is a correlation somewhere, but it may be too early to declare a pattern. Each one of these mini-crashes corrected the market by 57% to 77% of its original value.

In contrast, the dot-com doldrums lasted 19 months to be exact, from March 2000 until October 2002, when several companies lost 80-90% of their stock value, and many didn’t even survive. Interestingly, upcoming companies such as eBay and Amazon also saw their value drop significantly then, but recovered quickly thereafter. The dot-com crash did wipe $1.7 trillion in total market capitalization value for companies, but this is not a fair comparison because that included drops from large, established tech companies such as Cisco and Qualcomm, and not just the dot-com newcomers.

Here are some factors that make investing during this turbulent period challenging, but still interesting:

- Many companies get granted early liquidity, which isn’t always a good thing. Along with that, comes volatility as a risk itself, because the price fluctuations are speculation driven, and not performance related. So, the price movements caused by traders who are momentum chasers will give you false market signals.

- The Blockchain ecosystem has perfected the art of hype and expects that ideas, not results should be funded. Some entrepreneurs believe that the bigger the idea is, the higher the expectation of the funding requirement should be. And there is this false sense of entitlement that “token valuations” are the current norm, and that new, virgin projects need to inherit these similar multiples from the minute they are conceived.

- The laws of startup evolution and typical high failure rates will continue to apply for several reasons that Fred Wilson aptly enumerated in a post titled Drinking From the Firehose: “Some will fail to ship. Some will ship things that don’t work. Some will ship things that work but aren’t adopted. And some will ship things that are adopted but are surpassed by something better.”

- The fog has not cleared yet on the infrastructure and middleware layers. New players could still become dominant in the space within a two year period, given the right product is conceived. Moving sands can quickly reshape a beachhead.

- There are far too many pure crypto funds that operate like a hedge fund and they are speculating in a cryptocurrency market where it is too early to clearly discern the fundamentals that can be measured. The current system is loaded with promises, and there aren’t enough visible cases of blockchain usage to re-balance the scale between forward expectations and actual performance. We have clearly overshot expectations in this area. I'd like to see more projects with users, and more visible use cases going live. As I wrote earlier, we are in dire straits for token usage metrics to bring some sanity into how we could (better) evaluate some of these coins, A Guide for Blockchain Usage Metrics.

- Getting users is still the toughest part of blockchain projects. Not only do companies have to get their model right, they also need to get the token model to work properly. So, it’s a compounded set of iterations, interlaced with each other.

- Too many cover ups are difficult to detect. Any project that raised money in 2017 and still has no users or traction to show is probably headed to zero. A token offering is a lease on startup life. It keeps you afloat independent of VCs deciding to fund you or not. Extending your life doesn't mean you have a good life. In the absence of real accountability strings, self-assessment is not always good enough. Nobody will admit their baby is ugly. Sending them multiple times to the contest won't help them win.

For all of the above reasons, fundamental venture capital investing skills and experience will continue to be important, and not just the ability to get an early token discount in a private offering (so you can flip it), or figure out when a coin’s price will take off because some major exchange is going to list them.

There is hope that amidst this most severe correction, less babies are thrown with the bath waters, and that the better tokens re-bound faster than others. There are some gems and real diamonds in the ruff as well as ones that have yet to come out. We need a recovery where the good coins distance themselves from the not so good ones, just as the stock market rewards performance with varying degrees of valuation multiples that are not so arbitrarily granted to companies, but are based on deserving realities.

In sum, with the blockchain, good companies will continue getting created, out of each mini crash cycle. This was not the case with the dot-com crash when almost everything dried out for almost two years after the main crash. If you are an active investor, you're not going to get necessarily smarter by avoiding the battlefield, even as potential winners are sitting on the same roller-coaster ride as the ones that will get ejected along the way.

Yes, the blockchain can keep giving, but it will also continue bleeding.